What if I told you that you could get the discounts of a 3-year reserved instance, but with only 1-2 months of commitment? Better yet, what if your RI’s could auto-scale with your infrastructure demand? Believe it or not, it is possible. Come back next week when I share The NEW Ideal Portfolio

Many years ago, I inherited a cloud engineering team. The team had seen three other leads over the prior year, and almost 3/5 of the team had turned over in that same period. One of the first things I did was look at how effectively we were using our money. The steps I took then were the nexus of what has become my AWS Bill Triage service. Step 1 was to pull up cost explorer and look at RI and Savings plan coverage and Effective Savings Rate. What I found was, in the words of my CTO at the time, “almost criminal negligence”.

You can imagine how pleased my CTO, and later my CFO were when I told them we could save big money with little effort.

Getting Started with Commitment Discounts

Savings Plans and Reserved Instances are the cornerstone of any good cost management program. All too often, however, coverage is at 0! I’ve covered this before; there is really no excuse for not having at least some coverage.

What do you do when you’re just getting started? Well, it would be great to just immediately go get 100% coverage with 3-yr commitments and huge discounts, but that’s a bad idea for hopefully obvious reasons. An ideal portfolio of commitments is going to be much more difficult to build.

The (old) Ideal Portfolio

For many years I felt the ideal portfolio was one where an equal share of your reservations expired each month. This would give you the maximum opportunity to rebalance your portfolio each month. You would have a nice mix of 3yr and 1yr commitments with a mix of compute and ec2 savings plans and perhaps some standard Ris purchased on the marketplace to cover your particularly stable workloads. If we assume a workload dominated by Linux machines, your Effective Savings Rate (ESR) might be as high as 35% and your coverage might be as high as 80%. In some strategies, especially with relatively stable workloads, coverage could go as high as 100% with ESR in the low 40s. However, this ideal required almost 70% of your compute load to be covered with 3-year commitments, which doesn’t leave a lot of room for flexibility. Nonetheless, this type of portfolio is still better than probably 90% of companies have, so let’s talk about how to get there.

Building it out

One HUGE challenge with an ideal portfolio is that it takes a long time to build. In order to achieve high ESR, you need as many 3-yr discounts as possible. If you want to do this while maintaining monthly rebalancing options, you need to spread out your purchases for 3 years. That means I’m 3 years away from the portfolio I want. I can use the marketplace to try to overcome that, but that’s far from a sure thing.

Most organizations that are new to cost management find themselves having to make a choice between two options.

Option 1 – Save NOW

Under this approach you take the following steps:

- Buy as much 3-year commitment as you are willing to (typically maybe 50% of your current use)

- Buy as much 1-year commitment as you can on top of that (maybe that’s another 40% if you’re really aggressive)

- Wait a year and buy another 1-year commit

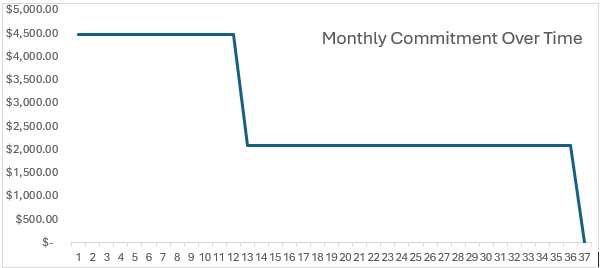

The good news is that you save money immediately, but the bad news is that any significant optimization gets frozen in it’s tracks because the savings have a hard floor. You end up re-balancing your commitments annually, which means you rarely try to reduce spending at all. Each year, your commit expiration profile looks something like this:

Essentially you have cliffs on an annual basis that represent 30-50% of your total run rate.

Option 2 – Save LATER

With option 2, we slow down with a focus on the long-term benefits of an ideal portfolio.

- Month 1 commit to 1-yr at 60% of your current run rate

- Every month, commit to 3-yrs at an additional 1/36th of your current run rate

- Month 13 commit to 1-yr at 30% of your current run rate

- Continue with the 3-yr purchases every month.

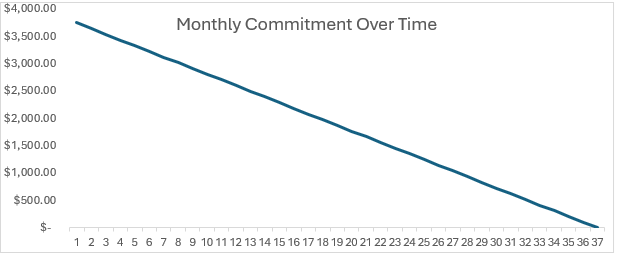

After 36 months, you’ll finally have a portfolio of 3-yr commitments that expire each month for the next 3 years. The tiered expiration dates give you a lot of flexibility to optimize and reduce utilization from month to month. Once you arrive, 3 years later, your commitment profile looks something like this:

Each month you’ll have about 3% of your commitment expire, leaving a lot of room for optimizations.

Is It Worth It?

It’s great to have this smoother commitment profile, and it allows you to have almost entirely 3-year commitments, but here’s the problem. How much money did you waste building that nice portfolio instead of having huge commitment cliffs? If you have a $1M on-demand ARR you’ll miss out on almost $120k in savings over those three years. On the other hand, in year 4 you’ll save $110k more. So, accounting for interest rates, you’ll break even sometime in year 5 by playing it slow. That’s a LONG time from now! Oh, and let’s not forget, you’re committed to between $700k and $1m over the next 3-years.

The Good News

Well, here’s the good news. You don’t have to choose. Next week we’ll talk about The New Ideal Commitment Portfolio, which puts both these approaches to shame, and better yet, I’ll tell you how you can get all the benefits without the commitment and without the wait. I guess that would make it The New Ideal Commitment Commitment-free Portfolio. If you just can’t wait, reach out and book an appointment and I’ll let you in on the secret today!